Vodafone case in a Nutshell:

In February, 2007

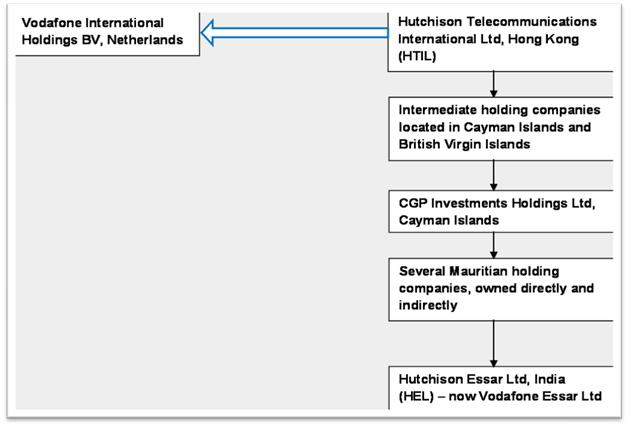

Vodafone (through its Netherlands entity) entered into an agreement with

Hutchison Telecommunications International Limited, Cayman Islands (‘HTIL’),

for acquisition of 66.9848% equity and interests in the Indian telecom business

of Hutchison Essar Ltd. (hereinafter referred to as ‘HEL’). The total value of the transaction was $

11.206 billion.

Since the transfer of the Indian telecom firm's shares and assets to Vodafone had led to capital gains for Hutch, the IT department demanded capital gains tax from Vodafone, which was liable to withhold this tax from the amount they paid Hutch. Vodafone claimed the transaction was not liable to tax since it was achieved by transferring the shares of a Cayman Island-based holding company and did not involve the transfer of a capital asset situated in India.

The High Court

rejected this contention by holding that “The essence of the transaction was a

change in the controlling interest in HEL which constituted a source of income

in India. The Petitioner (Vodafone) by the diverse agreements that it entered

into has a nexus with Indian jurisdiction. In these circumstances, the

proceedings which have been initiated by the Income Tax Authorities cannot be

held to lack jurisdiction.”

Vodafone

has filed an appeal before the Supreme Court against Bombay High Court

decision.

The Hon’ble Supreme Court vide its order

dated January 20, 2012 decided the issue in favour of Vodafone and held that

Vodafone was not liable to withhold any tax because no capital gains arose in

the said transaction which would be chargeable to tax in India. The Hon’ble

Supreme Court mainly observed as follows:

·

Section 9 covers only income arising

through a transfer of a capital asset situated in India; it does not purport to

cover income arising from the indirect transfer of capital asset in India. If

the word indirect is read into Section 9(1)(i), it would render the express

statutory requirement of Section 9(1)(i) nugatory.

·

Situs of shares situates at the place

where the company is incorporated and / or the place where the shares can be

dealt with by way of transfer.

·

Section

195 would apply only for payments made from a resident to a non-resident, and

not between two non-residents situated outside India.

·

The

entire transaction has been carried out outside India and in relation to

property which is situated outside India. It involves transaction between two

non-residents in respect of shares of a company incorporated outside India.

Therefore, the Indian Tax Authorities have no territorial tax jurisdiction over

the said transaction.

Proposed Amendment in Union Budget 2012-13 - A Retrograde Step

The

Government in its zest to establish superiority of legislature over judiciary

has now proposed the following major amendments in the Income-tax law

retrospectively from 01st April, 1962:

· In section 9(1)(i), to clarify that the word

“through” in the said section shall mean and include “by means of”, “in

consequence of” or “by reason of”. This explanation has been inserted with an

intent to provide that the income arising from indirect transfer of capital

asset shall also be included in section 9(1)(i).

· In

section 2(14), to clarify that the term “property” includes any rights in or in

relation to an Indian company, including rights of management or control or any

other rights whatsoever.

·

In

section 2(47), to clarify that ‘transfer’ includes disposing of or parting with

an asset or any interest therein, or creating any interest in any asset in any

manner whatsoever, directly or indirectly, absolutely or conditionally,

voluntarily or involuntarily by way of an agreement (whether entered into in

India or outside India) or otherwise, notwithstanding that such transfer of

rights has been characterized as being effected or dependent upon or flowing

from the transfer of a share or shares of a company registered or incorporated

outside India.

· In

section 9(1)(i), to further clarify that “situs of shares” of a company

incorporated outside India shall be deemed to be in India if the share derives,

directly or indirectly, its value substantially from the assets located in

India.

·

In

section 195, to provide that it will also cover payments made by a non-resident

to another non-resident. It has been further clarified that the said provision

will apply whether or not the non-resident has a residence or place of business

or business connection or any other presence in any manner in India.